")

")

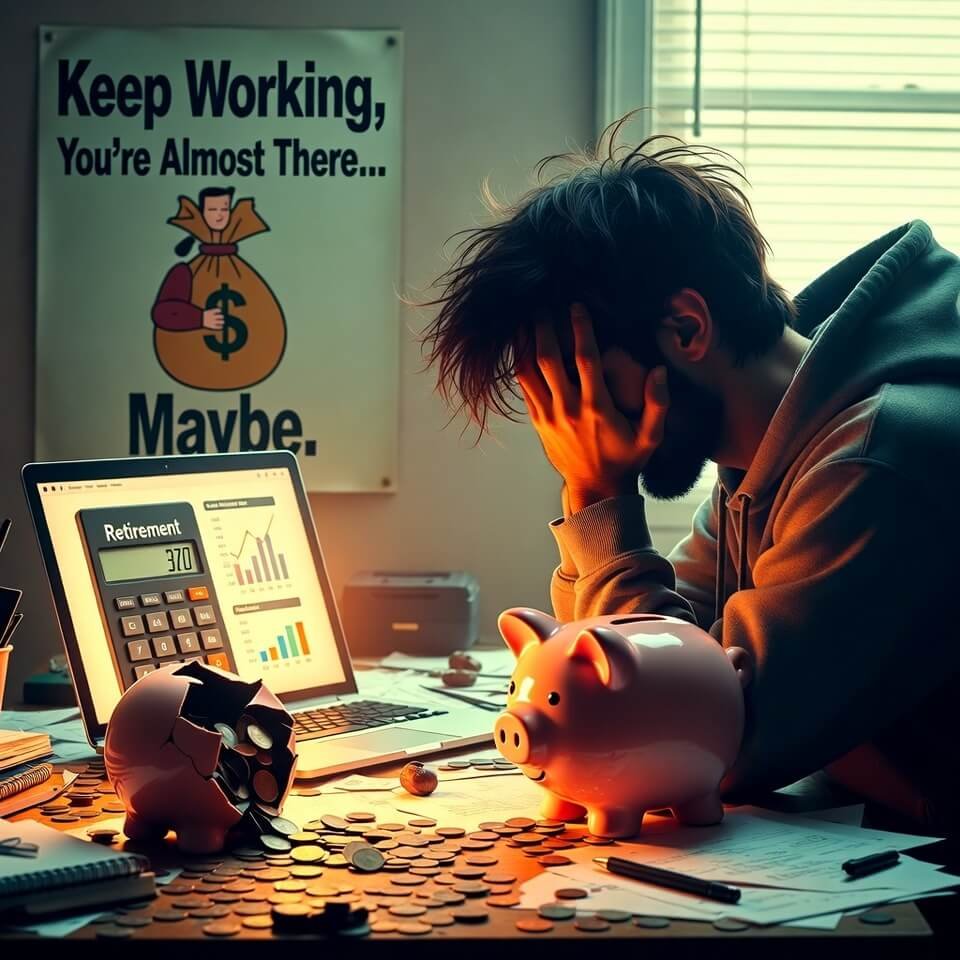

Okay listen… I just spent like four hours straight torturing myself with an early retirement calculator and I’m still kinda shaking.

Right now I’m slouched in my crappy apartment chair in [some mid-size US city], blinds half open so the street lights are making weird stripes across my keyboard. There’s an cold half-eaten burrito next to me, my phone keeps buzzing with work emails I’m pretending not to see, and my cat is literally sitting on top of my retirement spreadsheet printout like she’s trying to delete the bad news with her butt.

So yeah… I finally caved and ran the numbers. I used a couple different early retirement calculators (the one on Engaging-Persona FIRE Calculator and the legendary FIRECalc because apparently I hate myself) and holy crap the results were… humbling.

Why I’m Suddenly Obsessed With Early Retirement Calculators

I’m 34 going on “please god let me stop adulting soon.” I still get excited about new concert tickets but also panic when I see how much they cost. I want the freedom to wake up and decide I’m gonna write bad poetry, travel to weird small towns, or just lie on the floor staring at the ceiling for three days. That’s the dream, right?

So I started plugging everything into those early retirement calculators like it was my new full-time job.

My Real (Kinda Embarrassing) Numbers

Here’s the messy truth I put in:

- Age right now: 34

- Savings / investments: $87,432 (I feel both proud and deeply ashamed)

- Annual spending: ~$48,000 (I know, I know… too much oat milk lattes and vintage band tees)

- Safe withdrawal rate: 4% (the classic FIRE rule)

- Expected real return: 6.5–7% (I used to put 8–10% like an idiot)

- Current take-home pay: about $68k after taxes

I ran a few different scenarios:

- If I keep saving my current $1,400–1,600/month → Retire at 57–58 😭

- If I get serious and bump savings to $2,800/month → Drops to 49

- If I cut spending down to $36k/year AND save $3,200/month → … 43–44 ???

Seeing 43 made my heart do this weird fluttery thing… like maybe it’s actually possible? Then I remembered I still owe $14k on student loans and I impulse-bought a $300 mechanical keyboard last month. Back to earth.

Tools I Actually Used (Real Links)

These are the early retirement calculators that didn’t immediately make me want to yeet my laptop:

- Engaging-Persona FIRE Calculator – clean, easy to play with different scenarios

- FIRECalc – the scary honest one with historical data

- cFIREsim – great for seeing how bad things could get

- Vanguard Retirement Income Calculator – more boring but solid baseline

The Stupid Mistakes I Made (Learn From My Pain)

- Forgot healthcare would cost $12–18k/year before Medicare. Big oof.

- Used to assume 10% returns forever… lol no.

- Didn’t account for taxes on withdrawals from traditional accounts.

- Completely ignored inflation eating my future lifestyle.

- Didn’t include any “fun money” buffer for travel or emergencies.

So… How Soon Can I Actually Quit?

Realistically? If I stop being a dumbass with money and get aggressive, maybe late 40s. That still feels impossibly far away… but also closer than 60-something.

The early retirement calculator doesn’t lie, though. It just shows you the cold math. And the only ways to make the number smaller are:

- Earn more

- Spend way less

- Get stupid lucky with investments

- Or decide you actually need a lot less than you think you do

Which is both terrifying and weirdly freeing.

Anyway I’m gonna go stare at my sad cracked piggy bank (it’s missing an ear because I dropped it while drunk-dancing to Taylor Swift last year) and try not to have an existential crisis.

What about you? Have you run your numbers in an early retirement calculator yet? Did it make you feel hopeful, depressed, or both? Tell me your number or your biggest “oh crap” moment—I’m nosy and I need the solidarity.

Love you. Mean it. — Me, currently eating tortilla chips straight from the bag at 2:41 a.m.

")

{kind=link}